The Individual Mandate. Man, what a complicated and twisted path it’s taken.

Obama, himself, was against it before he was for it. in 2015, Vox said that it was “absolutely necessary” to making sure that Obamacare could be implemented. By forcing healthy individuals into the marketplace, it would lower the premiums for everybody else by spreading the cumulative risk around. If healthy people opted not to buy insurance, then the plan wouldn’t work.

The Supreme Court ultimately ruled by the slimmest possible margin that the mandate was constitutional—not because the federal government can force people to buy a product, but because the federal government does have the right to compel individuals to pay tax—undermining candidate and President Obama’s promise that taxes on the middle class wouldn’t be raised under his administration.

So, despite every liberal in the world screaming at the top of his lungs that President Donald J. Trump is a “moron” and an “Orange Droolius,” Trump beat the Democrats at their own game with his tax plan, which he signed into law earlier this month. Rather than try to “repeal and replace,” an effort which has failed massively in the Senate, Trump decided to simply repeal the individual mandate tax. Say what you want about the guy, this was some brilliant shit.

But did it kill Obamacare?

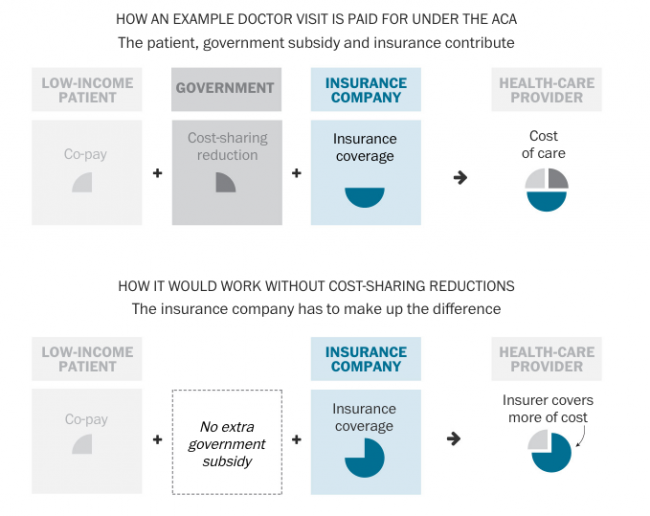

85 percent of projected Obamacare enrollees are eligible for subsidies, a strain on the federal budget that grew by 10 billion dollars in 2017. This is because the law was fundamentally broken—if insurance companies increase premiums, then the government simply paid them more money.

At the time of the 2017 subsidy increase, some red flags went up. “Since the premiums for 2017 are a lot higher than for 2016, it’s no surprise that premium tax credits would go up as well,” said Paul Ginsburg, director of the Brookings Institution health policy center, at the time. “The premiums in 2015 and 2016 appear to have been unduly low.” Gee, I wonder why. Couldn’t possibly have been to prop up Obamacare, could it?

Obviously no fan of the bill, Trump eliminated cost-sharing subsidies in October, saving $7-10 billion. And now that individuals who don’t want health insurance aren’t required to purchase it…who’s gonna cover these premium increases? It won’t be the federal government, thanks to the aforementioned elimination of cost-sharing subsidies. The state exchanges won’t have the budget.

So what will happen? Well, that’s where opinions differ.

Quite amazingly, some of the most rabid voices in support of the individual mandate are now saying that its repeal is meaningless. Some think that people will continue to buy coverage through the exchanges, even if they aren’t mandated to do so, because people would rather have health insurance than not.

However, what if the insurance companies opt out of the exchanges? This has already happened in shockingly high numbers—in fact, about 30% of current Obamacare enrollees will only have one choice for insurance in 2018. Aetna is leaving over 200 counties for 2018. Anthem is leaving around 400 counties. Humana is exiting about 150. And when you only have one choice, well, you don’t really have any choice at all.

At the current pace and in the current environment, where insurance companies are forced to cover more and more of the costs, it’s hard to see any of the larger insurance companies continuing to opt in for 2019 unless they’re given a compelling financial reason to do so. Under the current congress and administration, that seems unlikely. Obamacare fans are going to have to hope for a sweeping change in the midterm elections, and although democrat candidates currently have a double-digit lead over republicans in the polls, I seem to remember that Hillary also had a double-digit lead around this time in 2015, and Trump didn’t have the additional benefit of nearly 80 percent of Americans taking home an extra grand or two a year in their paychecks.

In the end, it seems likely that Mr. Trump will get his wish, that Obamacare will collapse under its own weight.

46 Comments

phase 2 already announced is to get inscos to introduce low cost no frills health plans. Clever.

It was doomed to fail from its inception but they will blame Trump for it. Single payer in the US is a non-starter for a several reasons.

Because people are stupid and don’t realize how much better off they’ll be with a single payer system.

I’m not going to argue with people being stupid. There are well moneyed, strongly lobbied, antitrust exempt interests that aren’t going to just walk off into the sunset if someone like Bernie wins and all three branches magically say we’re a British or Canadian model now.

That, and Americans, especially the generation hoovering up most of the health care dollars, are spoiled, self centered and won’t tolerate the rationing inherent to such a system, whether it’s implicit, or secondary to access shortages. The demographic bomb we’re sitting on won’t pay for it and neither will mass third world immigration.

The ACA succeeded in consolidating the big players, Insurance and hospitals, making them even more powerful and allowing both to increase their costs.

Doesn’t really matter Obamacare was a flawed law but it was better then doing nothing. pre Obamacare premium costs were already rising 3 to 4 times faster then inflation. If we go back to that plus no Gov subsidy your back to single payer being the only option (a version of Obamacare was the preferred option of the GOP for 20 years until a Dem passed it.)

By the way don’t give the Don to much credit on this one most reports seem to indicate Toomey as the one driving the push to kill the mandate

Don was pro universal healthcare until early 2016 when he got onboard with GOP calls to kill Obamacare to expand his base.

Obamacare was a tax.

Justice John Roberts passed it as a “tax”.

Obamacare was due to fail from the start simply because it required more revenue to stand that could possibly be generated in the amount of time required. “The individual mandate” was a tax. $700 or so. I know people who got hit with it. The Democrats were bad on the economy.

One thing’s for sure, with Trump in charge, my portfolios are doing better than ever. My marijuana stocks for example…off the chains.

I’ve seen 14% returns this year on my (very, I just started) investments.

Which is laughably high.

very small*

DAMN THE LACK OF AN EDIT FUNCTION

I’ve thought for a long time that simply arguing over who pays for healthcare is a dead end argument. The key to actual change in the healthcare market and the associated insurance is reducing the actual costs. Let there be more doctors enter the supply pool, allow more nurse practitioners to work on their own, give more transparency to what stuff actually costs and let me easily compare what different hospitals charge for the vasectomy/knee replacement/colonoscopy that I need to have done. Things like that would help lower costs and create good competition. Then healthcare and insurance would be more affordable for more people.

Exactly. There is a limit on doctors etc which could be lifted as long as Universities stick to set standards. This would reduce their exorbitant cost.

There’s no way in hell I could afford any kind of insurance for me or any of my family, and I was staring at being even more over the barrel with the individual mandate during this next tax season. It disappearing has been a huge sigh of relief for me.

Be careful as I understand it they kept the mandate for 2018 so you will need health insurance until 2019

“Quite amazingly, some of the most rabid voices in support of the individual mandate are now saying that its repeal is meaningless. Some think that people will continue to buy coverage through the exchanges, even if they aren’t mandated to do so, because people would rather have health insurance than not.”

That is a bit amazing. The providers in our area are hurting in a big way. Why? Because out of pocket costs are so high that folks are living with pain until it going to the Hospital becomes a necessity.

I’m still trying to figure out who exactly O-care was actually helping. An internal tally at the Hospital I work for shows more than 50% of the ED admissions are uninsured. I’m in Podunk Illinois, I can’t imagine it being much better in larger metro areas.

“I’m still trying to figure out who exactly O-care was actually helping.” It is helping exactly who it is supposed to be helping: big insurance carriers, pharmaceutical companies, medical equipment manufacturers, the electronic medical record companies (e.g. EPIC), Press Ganey (patient satisfaction score company that sells consultancy services to hospitals & clinics to game its own scoring system), the rapidly-expanding hospital administrator class, and medical debt collection agencies. Healthcare now represents 20% of US GDP and the US is spending way more money than the rest of the developed countries spend for substantially worse outcomes. So much of the debates about US healthcare devolve into arguments about premiums, payments, and taxes. Little of the debate is about outcomes. This country sucks in terms of dollars expended vs healthcare outcomes but the president of McKesson (evil healthcare company that is in top 10 Fortune 500 & #3 highest CEO pay). After having a baby in the US, mom is 3 to 6 times more likely to die than in France or Sweden (depends on region and skin color). Having spent 10 of the last 14 years working in Verdun-like conditions in healthcare, I can attest to the fact that we (the US) are dumping a ton of money for very bad outcomes. Healthcare in the US has devolved into a sick crony-capitalist, banana republic way of shaking money from a desperate public/taxpayers & into the hands of a kleptocracy that claims it has your best interests at heart. The inefficiency & profiteering is not a bug, it is a feature.

For every person who says how their premiums skyrocketed, I have heard someone else say that if it hadn’t been for the ACA they would be bankrupt for not having insurance when they were sick. It’s obvious that the it was flawed, but probably could have been fixed if there had been any effort to do so, instead of the 60+ repeal attempts.

But it’s all good now. By the way, where is that new healthcare plan that is “far less expensive and far better” and “covers everybody”? Still waiting…

I had insurance. Now I don’t. I know plenty of people in the same boat. Screw the people who weren’t paying their own way and sunk the people who were. Who is really greedy?

Like I said, it cut both ways, but nobody ever made an effort to fix it. Come on, over 60 partisan attempts to repeal knowing FULL WELL that each would get vetoed, but not a single bipartisan effort to fix it? But when the current president cries “obstructionist democrats” his cult eats it up like candy.

What it comes down to is that no one has even tried to fix healthcare, and once we return to the prior status quo it’ll be just as broken as it was before.

as someone who makes too much to get subsidies and who can’t get healthcare through work, i am totally screwed. my healthcare payments for a family of three are about the same as my rent. for that, i still have to pay out of pocket for everything. the only way you hit the deductible, is by getting hospitalized. oh and our real doctors (except thank god for our pediatrician) won’t take any exchange insurance. i was told when one doctor dropped us that the reimbursement rates are less than medicare and don’t come close to covering costs. there are no non-exchange policies available here.

the only good news is that the referral system is so convoluted that i usually can delay payment to the doctors for months because they keep screwing up the paperwork. i got out of a $2k bill one time because the morons refused to submit their bill properly no matter how many times i told them that i won’t pay until the insurance company approves the charge.

this is so messed up. please, please, please give us single payer.

We’re in a similar situation, being just slightly on the wrong side of the subsidy cliff. In my county Obamacare bronze costs around $1000 a month per person. That’s for the privilege of living under a $12000 deductible. Obamacare silver is $1379 a month. In my county it’s Blue Cross, take it or leave it. There’s no competition. The affordable care act is unaffordable for us. I don’t think that the elimination of the individual mandate will kill Obamacare but it will weaken it and I’m in favor of anything that brings down the personal budget busting Obamacare house of cards. I will never vote for any politician who has supported this scheme, for us it’s financial cancer.

Do you know of anything the government doesn’t wildly overpay for? It’s still all going to come out of your pocket, and don’t be surprised when ‘single payer’ has a sliding deductible to punish people who work for a living.

What, there are no other jobs/companies that have health insurance you could strive & apply for in your area?

Single Payer is bad for competition, both from a health care perspective and from an incentive to improve your lot in life perspective.

Insurance plans will always fail when they violate the definition of insurance. Insurance pricing is based on actuarial data that takes age, lifestyle, gender, and existing health into account to predict the likelihood that the customer will make a claim on the policy. Those with low probability will pay less than those with high probability, but in all cases the insurance market can only work if pricing is allowed to vary by risk and that the claim probability is less than 100%. Forcing insurance companies to sell health insurance at the same price to both those that are healthy and to those with pre-existing conditions is not insurance because the sick people have a 100% chance of making a claim. Forcing insurance companies to charge the young to pay the same price as the old is also not insurance because the prices do the correspond with the actuarial chance of making a claim. Thus Obamacare was doomed to fail from the very start because it tried to apply an insurance model to a non-insurance setting.

Cheaper healthcare with quality will only happen if most people pay for most healthcare out of their own pocket. Nobody is price sensitive if someone else (insurance or government) is paying the bill, and when nobody is price sensitive the service provider has no incentive to cut costs. If government really wants to help they should force all healthcare providers to provide prominently post their prices (which must be charged to all customers) for all commonly used health services so that comparison shopping can be done. If a hospital or clinic gets insufficient business because their prices are too high for the quality provided, they will need to figure out a way to cut costs or go out of business. 3rd party payers should be limited to catastrophic care, but even here the patient should have skin in the game that makes them sensitive to costs. If the 85 year old with cancer is required to liquidate a substantial portion of their estate to get an expensive experimental treatment with little chance of success before Medicare kicks in taxpayer dollars, I expect most of those patients will decide to go with the cheaper “pain-relief” option so as to leave some money for spouses and children. Healthcare will only get cheaper AND better when innovation activities are directed at not only better health outcomes, but also cheaper health outcomes, which is what you see in all medical areas such as cosmetic surgery and lasik eye surgery that most people pay for out of their own pockets.

This is the best comment I’ve ever read on this subject. No joke.

I hope it’s not, because ‘comparison shopping’ for medical procedures might be OK for a family doctor but its fucking stupid for anything non-voluntary. Unconscious people sure have a lot of choice in their health care.

The real issue is for-profit medical institutions. The people who run those institutions are the worst of humanity. Seeking to maximize profit off of people’s health is despicable.

Eric H – the vast majority of medical treatment is voluntary, and comparison shopping effects for those voluntary services will also lead to better prices for non-voluntary medical treatment because it will bend the cost curve down for the entire medical establishment. You are also wrong about profits – the best way to allocate scarce resources is the free-market system, where customers are free to spend their money at the places that provide them with the best service and value for money. Profitable firms in a free market are the ones that provide the best service/value, while unprofitable firms tend to be failures at one or the other or both, and the lack of profit is what gives them the incentive to improve with innovation. 75% of global medical innovation comes from the relatively “free-market” part of the US medical system, but the current system only rewards life-saving innovations, not cost-saving innovations – and we need both. It is always amazing to me that so many people seem to think the laws of economics don’t apply to health care, and think that government control is the answer – the same government that has bankrupt public pension plans, can’t properly maintain public infrastructure, and can’t run an efficient DMV.

Stingray we already know the government can run healthcare better. Medicare is less expensive and more efficient then private health insurance. (medicare runs at less then 5% overhead vs 12% for private)

Thanks Bark for the compliment and the thoughtful article that inspired it. Happy New Year.

Stingray has basically stated the classic conservative market theory. Which mostly has proven not to work on healthcare.Nobel winning economist Ken Arrow first wrote why in 1963.

https://web.stanford.edu/~jay/health_class/Readings/Lecture01/arrow.pdf

As already mentioned the basic issue is that the most expensive medical procedure tend to come at a time when you are not in a position to make good economic choices. If you tell me you can allow me to keep walking for another year but it’s going to cost 100K even if I have time to think about it i’m still going to spend the money I don’t have.

Then you talk about price sensitivity which is very true but in healthcare has bad effects. People simply delay or avoid care until it’s unavoidable and super expensive. Say my DR says I need to go to physical therapy but my insurance does not cover it. Instead of paying 90 bucks a week for it I wait until I now need surgery at 15k bucks. The math on charging out of pocket for basic care is bad. To look how this works ask yourself why dental insurance which is a lot less regulated the health insurance almost always pays for cleanings etc? Because if they catch things early it costs them less money.

We can also look at how the market works now with employer based health insurance. More and more money is being shifted to the consumer with higher deductibles and copays. Despite these changes the costs on these plan are still rising faster then inflation. Why it simply doesn’t work.

I actually agree on the published prices thing that would be great and maybe it would have fixed the HSA experiment that worked out rather poorly so far but I have my doubts (still willing to try it). To see why look at Singapore often held up as a free market example. There everyone puts money in tax free accounts and pays for basic healthcare with that money prices are published etc. Even with this system costs are not contained and there healthcare costs have been rising at 15% a year or more. No savings there.

Arrow may not have believed markets work for healthcare, but nobody has come up with a better alternative. Single payer systems tend to result in little innovation (they free-ride off US medical innovations), poor patient outcomes for serious illness (such as cancer), and long-patient waits for anything not deemed emergency. Anyone that argues differently is not comparing apples with apples. For example infant death rates are higher in the US because outside the US most infant deaths within the first few days are counted as “natural causes” and hence not counted in the infant death statistics as they are in the US. The US is also a multi-racial society, and blacks and hispanics have very poor health outcomes compared to whites and asians due to genetic and cultural factors that have nothing to do with the medical system. Thus comparisons of the US with mostly white France or mostly asian Japan leads to unfavorable results, but if you compare hispanic-Americans with Mexicans or Panamanians or black-Americans with black-South Africans or Kenyans or German-Americans with Germans you will see the US has better health outcomes by almost any standard. Anyone that says American should adopt single-payer should also ask themselves why such a system would be better than the dismal VA system that comes closest to single-payer in operation in the US.

The problem with health is that virtually everyone wants to live a good healthy long life and get whatever medical care necessary to make it happen, but far fewer are willing to pay the necessary price, including eating right, exercise, and the avoidance of bad habits such as smoking, drugs, etc. What will come closest to solving the problem of unlimited wants and limited resources is markets so that innovation and competition bring down the cost of that $100K surgery to $50K or $20K, and that $90 therapy to $35. The 2008 Oregon health experiment found that health insurance did not improve health outcomes, although it did increase healthcare service use, so the idea that paying out of your own pocket will decrease public health is not supported by evidence. Publication of prices, tax-free health savings accounts, mandatory or incentivized (tax-free) purchase of actuarial based catastrophic insurance from any provider including out-of-state, and tort-reform to reduce defensive medicine would truly have a magical effect on health care prices, AND encourage people to take better care of themselves (so they could keep more of their own money).

As I mentioned you can look at Singapore for published prices and paying out of pocket doing essentially nothing to control costs.

You look at the Oregon study is a bit one sided. While many health problems stayed the same the rate at which people were diagnosed with Diabetes and took medications for their long term ailments increased greatly which would seem likely to increase health outcomes long term. There was also a 16% drop in one year mortality rates among the study. Back in May there was an Article in the American Journal of health economics that studied long term effects of medicaid expansion since the early 2000’s they found a 6% reduction in fatalities from curable ailments as a direct cause of medicaid.

On the other points I agree the US is driving innovation in healthcare massive profits do that (well sometimes) I do fear that healthcare advances will slow because of it. But on a whole I’m much more worried that as 20% (well almost) of GDP the healthcare industry is single handily killing the rest of our economy.

Few more points. It’s not like no one is trying to control costs. Health insurance negotiates with providers for the best deals all the time, they deny crazy treatments etc. Even with that the costs of the plans still outstrip inflation. Look at it this way your basically saying a bunch of consumers with no negotiating experience would somehow come out better then teams of negotiators in reducing payouts? It’s really simple market forces have a minor and secondary effect on healthcare costs.

On the health outcomes Cuba has a better health outcomes then Hispanics in the US. (It’s about even with the white US population actually. ) Add to that that we spend far and away so much more then any other country on healthcare that if you add cost to the benefits we fall way way way down the ladder even comparing direct groups.

Not sure where you get your figures about Singapore from, but according to the Brookings Institute (left-wing) they have very low costs and very good outcomes (see link).

https://www.brookings.edu/wp-content/uploads/2016/07/AffordableExcellencePDF.pdf

As for Cuba, most honest assessments don’t rate their system very highly (see link), but of course Michael Moore gave the opposite impression. I also doubt that US doctors would be willing to work for $67 per month.

http://blog.acton.org/archives/90402-the-truth-about-cubas-health-care-system.html

Millions of consumers acting in their own self-interest has brought the price of cars, TVs, phones, jet travel, cosmetic surgery, etc. down dramatically, while quality has generally increased. Only things that the government puts their fingers in tend to increase in price and/or stagnate in quality (e.g. medicine, education). Insurance companies and government may have negotiating power, but in the end it still isn’t their money that is being spent, so the incentives are just not as strong as for the individual making their own decisions with their own money.

You have to look deeper at Sinapore. Healthcare has been my number one political items for almost 20 years now back when I was voting for Bush over Gore so I have spent time researching this.

Here is the short version. On the surface their system looks great a mostly hybrid system with most things paid from forced health savings accounts (about 10% of salary is diverted to them) and major medical issue taken care of with a form of government major medical. The system also uses private and government funded hospitals etc. When first started the system was affordable but offered no savings over previous medical systems as had been expected among free market theory types. Then additional cracks happened the private medical facilities focused only on what was profitable leaving the gov to fill in on all other procedures etc. This forced the government to regulate the private parts to force them to offer basic services to prevent strain on the public system. Costs still rose much faster then inflation so the government started price fixing certain things and forcing pay caps of medical staff. This kept it steady for awhile but now as Singapore population grows and ages they are facing major budget shortfalls and prices increasing at 12-15% a year. Which means they will catch up with the rest of the world in costs very shortly.

In all I would still be willing to try a system that’s similar but I have my doubts it would work.

On our system I’m curious what you would change?

Get rid of Employee plans?

Change all health plans to high deductible HSA plans?

Get rid of medicare?

Just curious.

As to having actuarial based plans, that’s well in good except most people over 45 would have a bit of trouble paying for them. It would also create an interesting effect with income inequality. While I’m not a believer in everything being equal I think there is a breaking point where the people get a bit angry I think letting them die in the st because they can’t afford healthcare might speed that up a bit. You can already see the start of it in the opiod crisis people with poor healthcare and poor opportunity literally dying in the streets.

stingray65……Correct me if Im wrong but it seems as though you think that those who are sick and can not afford medical care should be forced to die from lack of treatment because only those with enough money to pay should receive it. Regarding pre existing conditions should my 34 year old daughter who suffers from severe epilepsy, can not work, and has no choice but to live with us, be denied medical treatment because of her pre existing condition? If that were the case she would not be alive today. Your views, if I correctly understand them are selfish and cold blooded. Perhaps we should start euthanizing everyone who is sick and without funds. Sound familiar?

Rod Jones – People born with pre-existing conditions do not work for insurance – they need to be covered by a “high-risk” pool that is not funded by actuarial based insurance premiums. If you move too far away from actuarial based insurance premiums to subsidize the already sick, the price gets too high for the healthy and they drop out of the system and leave behind only the sick and poor as has happened with Obamacare. If you like single payer systems, you also have to remember that most single-payer systems were implemented when medicine was primitive and mostly about reducing pain while you die (young), which is not very expensive technology. Today we have medicine that can keep people alive almost indefinitely, which is very expensive and one reason that many single-payer systems around the world are suffering from insufficient funding that is manifested by long delays in treatment (often in the hope that elderly or chronically ill patients will die in the meantime) and often substandard care (see the US VA as an example). Unless medical systems can be designed to encourage cost saving innovations, any modern medical system is going to be increasingly faced with difficult decisions such as: how much should society spend to extend the life of an alcoholic or smoker with cancer, or an obese person with heart disease, or an 85 year old with dementia? Is the life of a low-income person with poor health habits worth the same “investment” in medical care as a low-income person with good health habits, or a higher income person that pays substantial taxes, employs people, and supports a family? Like it or not, these are the type of questions that need to be answered in an era when medical expenses can literally require a blank check. The question is – who should answer these life and death questions most of the time? If you like single payer then you are basically saying that you think some government death panel of “experts” should do it for everyone except the super rich, which means that the system will either provide mediocre care for everyone (to avoid making tough decisions) or provide good care for the most valuable patients and super cheap care for the non-valuable. Market advocates such as myself think the patient and their doctor should make most of these decisions, but only if the patient is informed about costs and has financial skin in the game, otherwise costs will never be contained.

Two things:

0. I’m definitely seeing that “delay of care” as regards my Army-vet mom whose sarcoidosis and lung failure seem to have a VA “treatment plan” of having her wait six months between doctor visits in the hope she’ll just drop off;

1. A while ago, the “spy photographer” Brendy Priddy posted this long Twitter rant about how “I NEED $4000 OF MEDICATION A MONTH AND THE BEST ANY INSURANCE PLAN CAN DO FOR ME IS A $2400 MONTHLY PREMIUM OMG.” All I could think of was, “What insurer is stupid enough to sign up for a guaranteed $1600/month loss?”

Well in all likely hood their negotiated rate on the prescription is likely much lower plus you have the grouping effect. An old school actuary would avoid writing a policy on some one with 20,000 accident for less then 5k a year but now a days with large risk pools almost all of them will do it for a couple grand a year.

For myself and most of the population that showing little to no wage growth living paycheck to paycheck I think most would take a chance on mediocre care with zero chance of bankruptcy then the opposite.

It is not the best comment by a long shot since it is wrong. But people only want to believe what fits their own bias.

“Forcing insurance companies to charge the young to pay the same price as the old is also not insurance because the prices do the correspond with the actuarial chance of making a claim.”

If you are going to argue and try to convince people you should know the facts but then again it doesn’t fit the narrative here. Rates on the ACA are NOT the same for young vs old. According to the ACA site: “Premiums can be up to 3 times higher for older people than for younger ones.” Is that enough of a spread? I don’t know but it’s not “the same”

Obamacare forced insurance companies to severely compress the rates they charge different groups, so yes the old could be charged 3 times more than the young, but that is a far smaller difference than actuarial based chances of making a claim. Same with gender as women make more medical claims and traditionally have been charged more for health insurance, but Obamacare banned gender based differences in pricing. Since young people tend to have the lowest incomes, and often have big debts from education and other loans, it isn’t really fair that they are asked to subsidize the older population that typically have far higher income and assets, but that is what Obamacare forced insurance companies to do – and guess what? Only sick younger people signed up for Obamacare, because they also benefit from the subsidies, but healthy young people have stayed away in droves.

Bias is when you ignore economic realities by assuming everyone has a right to unlimited medical care at someone else’s expense.

You need to take Obamacare into context of who wrote it. Most of it was written by the insurance companies themselves it was basically their idea.

Forcing everyone to buy health insurance — Industry idea

Grouping large age swatches together to charge more — Industry idea

The real deal story is this. Health insurance and Government got together and birthed the idea that there was millions of healthy people with out insurance and if we got them all onboard getting the sick on too would make it work. In actuality the percentage of the healthy population uncovered by their parents or employers health insurance was pretty small.

The largest group of uninsured is actually those 26-44 years old. Younger then that has higher rates of coverage.

Basically their numbers were wrong. Many of those now uninsured were uninsured pre obamacare when they could buy lower coverage cheaper plans that lacked gov subsidies. Neither carrots nor sticks brought them in free market won’t either.

Most people complain about the coverage they get on their federally mandated plans now (high deductibles high copays) the idea that they would be happy paying for subsidized bare bones plans better seems highly unlikely for the majority of the individual marketplace (which would be why more people are insured now then back when)

Prior to Obamacare, the overwhelming majority of people in the private health insurance market were happy with their insurance plans, which is why Obama lied and said “if you like your current plan you can keep your current plan….”. The minority of people that were not happy were those with pre-existing conditions and/or very low incomes and a high probability of needing medical care due to age or bad habits, who either couldn’t get/afford coverage or were paying way more than they wanted. So Obamacare flipped the whole market on its head to force all those that were happy and healthy to buy shitty over-priced insurance that would hopefully be so profitable for insurance companies they could afford to provide subsidized plans for the unhealthy minority that had previously been unhappy. The insurance industry only wanted to force everyone to buy insurance because that was the only way it MIGHT work out financially when they were being forced by Obama/Dems to insure everyone from stage 3 cancer patients to marathon runners for basically the same price (only minor variance allowed). Believe me, Obamacare was NOT the idea of the insurance industry, they were only trying to make the best of the very bad hand that Obama/Dems were forcing on them. Sort of like forcing someone to play Russian Roulette and letting them choose whether they want 4 or 5 bullets in the six-shooter.

Here are the origins of the mandate and pooling that ACA came up with

Newt Ginrich Meet the Press 1993

“I am for people, individuals — exactly like automobile insurance — individuals having health insurance and being required to have health insurance. And I am prepared to vote for a voucher system which will give individuals, on a sliding scale, a government subsidy so we insure that everyone as individuals have health insurance.”

This came from a plan then being passed around by Phil Gramm (R Texas) around the same time Clinton was pushing for a health overhaul.

Here is what it called for

Require all employers to offer a group plan

Require everyone have Heath insurance

No denial for prexising conditions (thou rates can be adjusted within a federal guideline)

All plans must meets federal minimum definitions for coverage and cost

Tax credits/ Vouchers for poor and working poor

Sounds awfully familiar

Then you have Romney care introduced in 2006 which really is 90% of the ACA right down to the subsidized state marketplace with minimum coverage plans. Also Pre existing conditions were thrown out just like the ACA. Thou as I understand it they gave a bit more flexibility in age rating but did eliminate gender rating just like ACA.

On a side note I was at a holiday dinner a number of years ago with a coworker who’s husband was a technical writer for a large health insurer. He says there are whole paragraphs of text in the ACA that were literally written by his company (that he proofread) that were inserted by their lobbyists that made it into law.

Romney has been quoted as saying his concepts for Romney care came from calling the heads of Health insurance and asking them what to do and that’s what he got.

So what we really have was a GOP/Helathcare industry plan to change health care that had a health dose of spending and medicaid tagged on by Democrats.

It is likely one of the most bipartisan pieces legislation passed in the last 15 years but no one will admit it.

I’m not saying Obama care is the answer far from it. I think it’s a hugely flawed plan that was destined to fail eventually. But I always hoped it would be a stepping stone to something better.

On a side not Obama did indeed lie. Quite a few times on the ACA in particular. They killed certain high deductible plans that were popular with certain self employed types and I will admit there is likely still a market for those.

He also lied when he was running saying he wouldn’t support the insurance mandate

He also lied saying there would be a public option.

Again not great but it was a start.

First, let me say I appreciate the intelligent dialog with out ‘liberal’ this and right wing’ that being bandied about. Best debate I’ve read in a while and I came to a sudo-automotive blog to find it.

There are great points on both sides with no one really coming up with any answers.

I’m curious about the thoughts of pulling the profit out of the insurance companies and how that would effect our costs and our employer costs across the board. Seems to me, some of the costs associated with the plans are so those in the upper echelons of the industry are well compensated. Not to mention the millions it must take to lobby for all these laws, etc. for both sides.

We should not be leaving the ones who can’t afford healthcare to just die in the streets, we are a modern society and should be able to find a solution. The problem, as I see it, is always the money.

Freekcj – there isn’t much profit to be taken out of health insurance companies – they average about 3% returns. To take big costs out you have to attack the medical service cost structure, and the most effective way to do that is through competition, innovation (in technology, treatment, and administration), and deregulation, and the best way to provide incentives for competition, innovation, and deregulation is for more consumers to pay for more of their medical expenses out-of-pocket. See the link for an example in Oklahoma, where a cash only clinic charges 50% or less than a typical clinic for various types of surgery, mostly because they need a far smaller administrative staff since they don’t need to deal with insurance companies or Medicare/Medicaid.

http://time.com/4649914/why-the-doctor-takes-only-cash/

Mopar: I am enjoying our debate on what is obviously a very difficult issue. My answers to your earlier questions all revolve around the overall idea that a system needs to encourage not only better service and technology, but also cheaper:

On our system I’m curious what you would change?

1. Get rid of Employee plans? – ANSWER: Ideally yes I would get rid of them. To make what Newt Gingrich and Republicans suggested in the 1990s work really required getting rid of employee plans so that everyone would get in the same basic pool, but the unpopularity of that is why it never happened. Short of that, I would not allow employee health plans to be tax deductible business expenses, which would get most firms out of the health care business and likely shift most of the money spent on health insurance to higher employee salaries (which would still be deductible). I think people would be very surprised by how much their salaries would jump under such conditions.

2. Change all health plans to high deductible HSA plans? – ANSWER: Mandatory or incentivized Health Savings Accounts are great because they make individuals responsible for their own spending (skin in the game), and when combined with cheap high deductible catastrophic insurance, provide protection against bankrupting major medical costs. Low income people could be automatically enrolled in a basic plan and have their HSA accounts topped up with sliding scale based on income using something similar to the Earned Income Tax Credit type mechanism.

3. Get rid of medicare? – ANSWER: Yes and Medicaid and the VA. A simple mandatory/incentivized (tax-free) enrollment in a HSA program and basic catastrophic insurance should be the model for everyone. Veterans could be provided with a generous catastrophic plan and HSA help as a replacement for the VA, which would allow them to go wherever they can get the best help. Annual HSA allowances/contributions could be raised or lowered to compensate for actuarial based differences in likely claims due to age and gender differences. Catastrophic insurance rates should also be actuarial based, with basic plan benefit limits reduced during senior years to keep prices down. Congress and their staff and other government officials MUST be enrolled in the same plan that is mandated for the public. Wealthier people would be free to use their own after-tax money to buy more generous plans and insurance companies would be allowed to sell all plans across state-lines to increase competition.

Other suggestions:

4. Mandatory publication of prices for all major medical services. Everyone gets the same price (no group discounts). I might also strongly encourage some national database of patient satisfaction scores by type of medical issue for all medical facilities, so that patients can compare both price and quality.

5. Tort reform – limiting malpractice awards to reduce defensive medicine.

6. Funding for increased medical school and nursing school enrollments to increase the supply of medical professionals. Deregulation of medical markets to allow nurse practitioners to do more medical treatments, allow sale of insurance across state-lines, allow remote or robotic medical treatment options. Increased government funding for research on cost saving innovations.

7. Retraining of all medical staff and administration in being honest with patients about treatment costs and outcomes. To keep costs down for everyone, heroic (i.e. low probability of success) and costly treatments will likely need to be replaced by pain management treatments for many people whose medical conditions are due to poor life choices, and/or who are not productive members of society. I shudder to think how much money California taxpayers spent to keep Charlie Mason alive during his old-age related illnesses, but something like 25% of lifetime medical expenses are spent during the last year of life of senior citizens. If an elderly sick senior citizen is wealthy and/or has accumulated a large sum in their HSA over many years of healthy living, and wants to spend their own money on a heroic and costly treatment, they should have a right to spend all they want, but they should make that decision based on knowing the probability of success. On the other hand, there has to be a line drawn somewhere on using public expenditures to extend the life of elderly people without those personal resources by only few days or months.

Few thoughts.

I agree on dumping employer based health plans I think they are warping the market.

I would be willing to try another run at HSA with published prices but after our initial experiments with them in this country I have a feeling it would do little to actually stop out of control medical spending but I’m willing to try it before we go all Canada.

Tort reform sounds good but seems like it won’t do much based on Texas which based tort reform. In taxes it did nothing to lower costs to consumers but did seem to give DR’s and insurers much healthier returns. Which isn’t what most economists would tell you would happen but the data is there and that’s what happened (another reason I believe markets have little effect on health care)

I think the point about controlling senior healthcare costs will never happen. One you have people like me who believe healthcare should be a right ( most polls put this position being held by 50-60% of Americans. ) You then have the practicality of passing something politically Seniors are an incredibly powerful political group and they are not going to accept medicare going away. The fact that medicare exists is proof of the fact that Americans want their seniors taken care of well medically with little likely hood of bankrupting them.

Tort reform is going to have a slow effect due to the build-up of the medical-industrial complex that has come from rampant and crazy malpractice awards. All the medical testing clinics that been built to run the tests that protect against lawsuits, which are often owned by the doctors ordering the defensive tests, aren’t going to go away immediately with tort reform. The fancy (and costly) hospitals that have been (over)built on “generous” third-party paid fees also aren’t going to go away immediately, but incentives have to be aligned to start turning the costs in the other direction.

As for poll support for “healthcare as a right”, it all depends on how the questions are asked. If you ask people to agree-disagree on “Everyone has a right to get the healthcare they need” – a majority of people will agree. If you ask people if “those born with health defects that mean they can’t afford insurance should get the healthcare they need” a majority are again going to agree. But if you start bringing in personal responsibility or cost shifting then agreement rates will plummet for questions such as – “The public should pay for the $100,000 liver transplant of an alcoholic without insurance”, “I don’t mind if my health insurance rates double in order to subsidize those that can’t afford it”, “Tax dollars should be used to provide healthcare for illegal immigrants”, “Tax dollars should pay for a $50,000 medical treatment of an elderly patient, even if it extends life by only a few weeks.” Healthcare can only be a right if it doesn’t bankrupt the others who are paying for it. Is food a right? Most people would say yes, nobody deserves to starve. But when you start saying everyone deserves gourmet meals made from expensive exotic ingredients, you will get far fewer people agreeing to pay for the starving person’s meal. That is the problem with making healthcare a right, because we either have to be willing and able to withhold some available treatments from those that can’t pay, or we have to find ways to make available treatments much cheaper so they are more affordable to patients that pay their own way and/or those of us that subsidize those who can’t pay.